Hafiza Ayesha Waheed

Hafiza Ayesha Waheed

The first Self Assessment tax return is a rite of passage that almost nobody enjoys and very few people feel prepared for. It arrives — or rather, the awareness of it arrives — as a low-grade anxiety that starts somewhere around October and builds steadily toward January, when it becomes something closer to dread. What do I need to include? What can I claim? What if I get something wrong? What is a payment on account and why does my bill look 50% larger than I expected? Why does the HMRC website look like it was designed to be confusing on purpose?

These are not the concerns of disorganised people. They are the concerns of millions of UK sole traders and freelancers who have done good work, earned money, and now face a tax system that assumes familiarity with processes, terminology, and deadlines that nobody explained to them when they went self-employed. According to research from Taxfix, 16% of UK freelancers are actively reconsidering self-employment specifically because of tax stress. A further 19% said they would rather pay the £100 late filing penalty than deal with the process at all. Around one million people missed the 31 January 2026 deadline entirely. If any part of that sounds familiar, this article is for you.

Why the First Return Is the Hardest

The self-employed tax return is not complicated in the sense of requiring specialist knowledge. It is complicated in the sense of requiring you to know things that nobody told you, in a sequence that is not obvious, using terminology that is inconsistent with the way ordinary people think about money. The combination of unfamiliarity, high stakes, and HMRC’s notoriously confusing website — cited by 54% of respondents in the Taxfix survey as the main reason for delaying their return — creates the kind of paralysis that turns a manageable admin task into a months-long source of stress.

The first return is also the one most likely to contain the errors that cause the most lasting problems. Payments on account — the advance payments HMRC requires toward the following year’s tax bill — are a standard feature of the self-assessment system that the majority of first-time filers have never heard of until they see their January bill and find it is one and a half times what they expected. Missing allowable expense deductions means paying more tax than necessary. Incomplete income reporting, even accidentally, means HMRC follow-up later. None of these are events you can reverse after the deadline.

The number that explains the anxiety

11.48 million people filed their Self Assessment for 2024/25 on time in January 2026. Around one million did not — and every single one of those now faces an automatic £100 penalty, followed by daily charges of £10 per day from three months late, up to a maximum of £900, before further percentage-based penalties begin. The deadline is not a suggestion.

The Penalty Structure You Need to Understand Before Anything Else

HMRC’s Self Assessment penalty system is automatic. There is no discretion, no warning letter before the first penalty, and no exemption for first-time filers who missed the deadline through genuine confusion rather than deliberate avoidance. The penalties apply even if you owe no tax at all — even if HMRC owes you a refund. Understanding the structure is not optional for anyone who is self-employed in the UK.

Deadline Missed By | Penalty | Notes |

|---|---|---|

1 day (from 1 February) | £100 fixed penalty | Automatic; applies even if no tax is owed or a refund is due |

3 months (from 30 April) | £10 per day, up to 90 days | Maximum additional £900 on top of the initial £100 |

6 months (from 31 July) | 5% of tax due or £300, whichever is greater | Applied on top of all previous penalties |

12 months (from 31 January following year) | Further 5% of tax due or £300, whichever is greater | Potential total in thousands before interest charges |

Late payment (30 days) | 5% of unpaid tax | Separate from the filing penalty; both apply simultaneously |

Late payment (6 months) | Further 5% of tax unpaid at that date | Compounds on the outstanding balance |

Late payment (12 months) | Further 5% of tax unpaid at that date | Daily interest also accrues throughout at HMRC’s current rate |

The critical point for first-time filers is that the filing penalty and the payment penalty are separate and both apply. A sole trader who misses the January deadline by six months and also pays late has accumulated the £100 initial penalty, up to £900 in daily penalties, a 5% payment surcharge at 30 days, and a further 5% payment surcharge at six months — all on top of the original tax owed, which is itself accruing daily interest. The total exposure from a missed deadline is not a minor inconvenience. For a first-year trader with a tax bill of £4,000, a six-month delay adds well over £1,500 in penalties and interest before any reduction for prompt payment.

The Ten Things That Trip Up First-Time Filers

The mistakes that cause the most problems for first-time Self Assessment filers are not random. They follow a consistent pattern, documented by accountants who see the same issues every January. Understanding them before you file — ideally before the tax year ends — is the difference between a straightforward return and an expensive correction exercise.

Not registering for Self Assessment early enough — you must be registered before you can file. HMRC’s registration process issues a UTR (Unique Taxpayer Reference) number by post, which takes weeks. Registration for self-employment must be completed by 5 October following the end of the tax year in which self-employment began. Missing this creates a cascade of deadlines you cannot meet.

Assuming only “main” income needs declaring — all taxable income must be declared: side hustles, freelance work, gig economy earnings, income from online selling above the £1,000 trading allowance, and interest above the Personal Savings Allowance. HMRC data-matches from multiple sources and will identify undeclared income.

Not claiming all allowable expenses — first-time filers typically either claim nothing (out of fear of getting it wrong) or claim incorrectly. Allowable expenses for self-employed people include a proportion of home office costs, mileage, professional subscriptions, software, training directly relevant to the business, and advertising. Underclaiming is paying more tax than the law requires.

The payments on account shock — if your tax bill exceeds £1,000, HMRC requires advance payments toward the following year’s bill. These are due in two instalments: 31 January and 31 July. In the first year, the January payment includes the full year’s tax bill plus the first payment on account — meaning the effective total due in January is 150% of what many first-time filers expected to pay.

Misunderstanding Class 2 and Class 4 National Insurance — self-employed people pay both. Class 2 (now collected via Self Assessment for most) and Class 4 (9% on profits between £12,570 and £50,270, then 2% above) are additions to income tax, not alternatives to it. Many first-time filers calculate their expected bill based on income tax alone.

Missing the overlap between employment and self-employment income — people who are both employed and self-employed need to include both the P60 income from their employer and their self-employment income on the same return. The tax code on the employed income affects the calculation for the self-employed element.

Estimating rather than recording — when records have not been maintained during the year, it is tempting to estimate. Estimated figures that do not match bank records, invoices, or payment platform data trigger HMRC compliance enquiries. An enquiry that could have been avoided with correct records can take months to resolve.

Filing in the final hours of January — 475,722 taxpayers filed on the last day of January 2026. Any technical issue, any incorrect figure noticed too late, any HMRC system slowdown becomes a penalty risk. Filing in December or early January removes that risk entirely.

Not understanding the tax calculation HMRC produces — HMRC’s calculation of what you owe can differ from what you calculated. The reasons — corrections to allowances, adjustments from prior years, differences in NIC treatment — are not always explained clearly. Not reviewing the final calculation means potentially missing a discrepancy that should be challenged.

No real-time picture of the tax liability during the year — the most expensive mistake is not any single error on the return. It is arriving at January without enough money set aside to pay the bill. Without a running estimate of the current tax liability, based on actual income to date, most self-employed people discover what they owe at the same point as the deadline.

What Making Tax Digital Changes for Self-Employed People

From 6 April 2026, self-employed individuals and landlords with qualifying income over £50,000 are required to use Making Tax Digital for Income Tax Self Assessment. This replaces the single annual return with a system of quarterly digital updates to HMRC, followed by a year-end final declaration. The threshold drops to £30,000 from April 2027 and £20,000 from April 2028.

For the 850,000 sole traders and landlords in scope from April 2026, this means the traditional January panic is structurally replaced by a quarterly rhythm. Records must be kept digitally and updated continuously rather than assembled once a year. Quarterly summaries of income and expenses are submitted to HMRC through compatible software — not a full tax return, but a real-time update that keeps HMRC informed of the current position throughout the year. The final declaration at year-end confirms the numbers and completes the process.

The psychological shift this creates is significant. The annual tax return is stressful in large part because it requires reconstructing 12 months of financial activity in a compressed window under deadline pressure. The MTD quarterly model distributes that work across the year in smaller, manageable segments. The business owner who keeps records current in Sage throughout the year arrives at each quarterly deadline with the work already done — and arrives at the year-end declaration needing only to review and confirm, rather than to compile from scratch.

How Sage Removes Each of the Problems

The specific features of Sage that make Self Assessment manageable are not abstract. They map directly onto the problems that cause first-time filers the most difficulty — and in each case, the software handles the problem automatically rather than requiring the user to remember, calculate, or decide.

The Problem | Without Sage | With Sage |

|---|---|---|

Tracking income throughout the year | Bank statements, invoices, PayPal exports assembled in January | Every income transaction recorded and categorised in real time via bank feed and invoicing |

Identifying allowable expenses | End-of-year guess-work; typically underclaimed or incorrectly claimed | Expenses categorised transaction by transaction; Sage Copilot suggests category for each entry |

Knowing the tax liability during the year | No visibility until accountant or HMRC calculates at year-end | Real-time tax liability estimate updated continuously from actual income and expenses |

Payments on account planning | Discovered on the January bill; often not budgeted for | Payments on account visible in the tax estimate; set-aside notifications available |

Receipt and expense documentation | Receipts collected, lost, or submitted incomplete at year-end | Sage mobile app photographs receipts at point of purchase; AutoEntry extracts and matches |

MTD quarterly submissions (£50k+ income) | New obligation, unclear process, separate login and software required | Quarterly updates submitted directly from Sage to HMRC; same interface as daily bookkeeping |

Year-end final declaration | Full reconstruction of the year’s records under January deadline pressure | Year-end is a review and confirmation of records already compiled throughout the year |

Mileage tracking | Manual log or year-end estimation; frequently underclaimed | Sage mileage tracker logs journeys with purpose; calculates HMRC approved-rate deduction automatically |

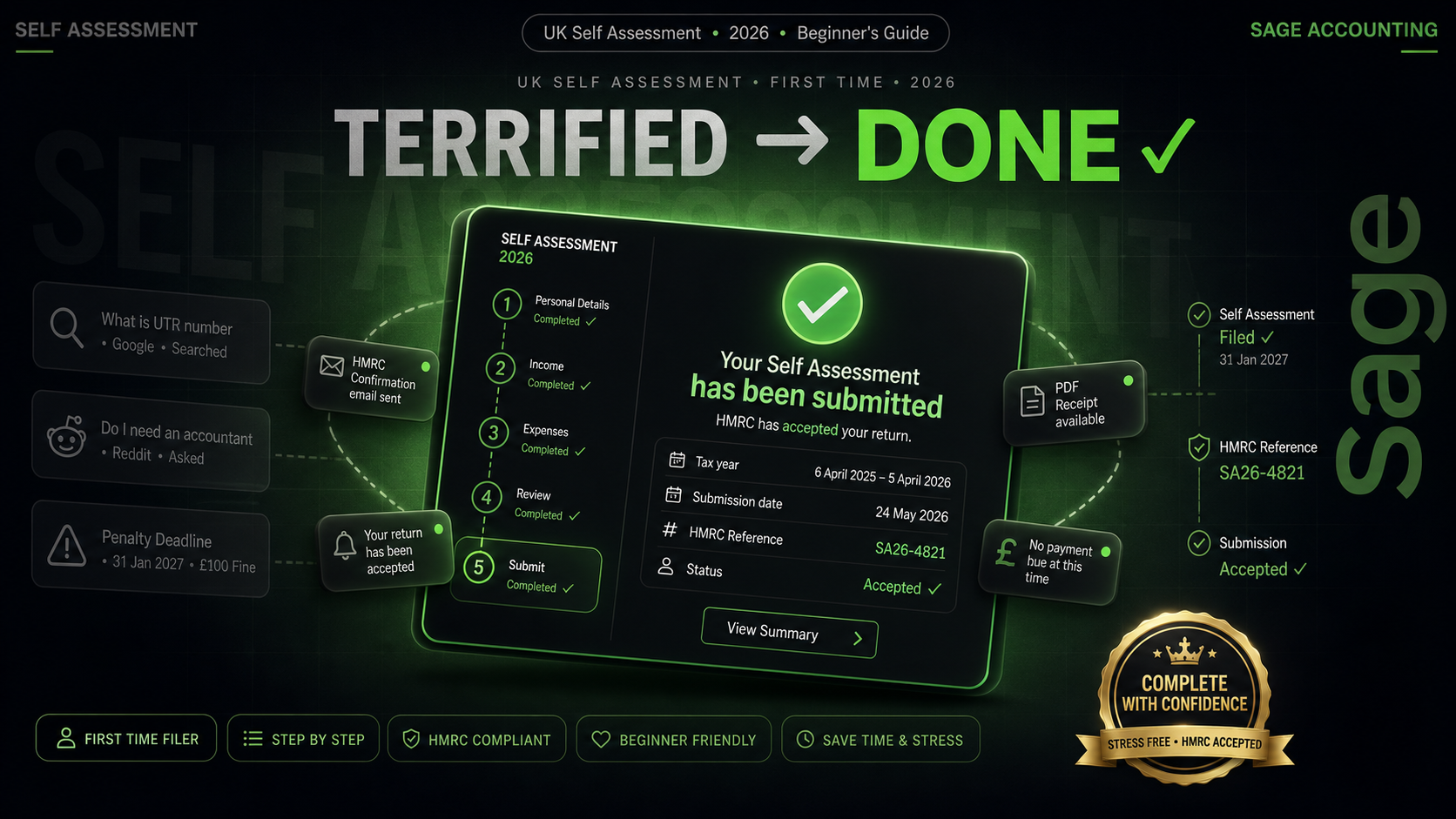

The Real-Time Tax Estimate: The Feature That Changes Everything

Of all the features that make Sage genuinely useful for self-employed people managing their own tax, the real-time tax liability estimate is the one that most directly addresses the anxiety. It does not just tell you what you earned. It tells you — continuously, from the data already in the system — approximately how much tax you are going to owe at the end of the year based on what you have earned so far.

That single number, updated automatically as invoices are raised and expenses recorded, transforms the tax return from a January surprise into a known quantity that has been building in a corner of the screen for twelve months. The self-employed person who has seen their estimated liability grow from £2,400 in August to £3,900 in November to £5,200 in January arrives at the return date already knowing roughly what to expect and — if they have been setting money aside based on the estimate — already holding the money to pay it. The person who had no running estimate arrives at the same point with the same bill and no preparation.

The payments on account problem disappears almost entirely with a running tax estimate. Rather than discovering in January that the bill is 150% of the expected amount, Sage’s estimate includes the projected payments on account in the calculation so that the total January liability is visible months in advance. The shock that catches hundreds of thousands of first-time filers every year is, with the right software, not a shock at all. It is a figure you have been watching grow since the first invoice of the year.

Before and After: Two Ways to Experience Self Assessment

Without Sage

October: Realise the January deadline is approaching; feel vague dread

November: Collect invoices, bank statements, and receipts from across the year

December: Try to reconstruct income and expenses from incomplete records

January: Panic-file in the final week; rush increases risk of errors

January bill: Discover payments on account make the total 50% higher than expected

February: Receive HMRC query about an income figure that does not match their data

No running total: No idea what the tax liability is until the return is prepared

Expenses: Underclaimed out of uncertainty; overpaying tax for years

With Sage

Ongoing: Every invoice and expense recorded in real time via bank feed and mobile app

Ongoing: Real-time tax estimate updated automatically; payments on account included

Ongoing: Receipts photographed at point of purchase; no year-end receipt hunt

Quarterly (MTD users): Update submitted directly from Sage; 15-minute task

December: Records are already complete; year-end is a review, not a construction project

January: Final declaration confirms the numbers already in the system; no surprises

January bill: Expected figure; money already set aside based on the running estimate

Expenses: Every allowable expense captured and categorised; no underclaiming

Self Assessment Key Dates for 2025/26

Date | What It Is | Who It Applies To |

|---|---|---|

5 October 2026 | Deadline to register for Self Assessment for 2025/26 | Anyone newly self-employed in the 2025/26 tax year |

31 October 2026 | Paper Self Assessment return deadline | Anyone submitting a paper return for 2025/26 |

31 January 2027 | Online Self Assessment return deadline for 2025/26 | All Self Assessment filers; MTD users submit final declaration instead |

31 January 2027 | Payment deadline for 2025/26 tax plus first payment on account for 2026/27 | All Self Assessment taxpayers with a bill over £1,000 |

31 July 2027 | Second payment on account for 2026/27 | All Self Assessment taxpayers making payments on account |

7 August 2026 | First MTD quarterly update deadline (Q1: 6 April–5 July) | Sole traders and landlords with qualifying income over £50,000 |

7 November 2026 | Second MTD quarterly update deadline (Q2: 6 July–5 October) | Same as above |

7 February 2027 | Third MTD quarterly update deadline (Q3: 6 October–5 January) | Same as above |

7 May 2027 | Fourth MTD quarterly update deadline (Q4: 6 January–5 April) | Same as above |

The Bottom Line

The fear around the first Self Assessment return is not irrational. The process is genuinely unfamiliar, the penalties for errors or late filing are real and automatically applied, and HMRC’s own systems are widely experienced as confusing — a finding confirmed by more than half of respondents in Taxfix’s survey of 2,000 UK freelancers. The fact that around one million people missed the January 2026 deadline, and that 16% of freelancers are reconsidering self-employment specifically because of tax stress, reflects a real problem with real consequences.

But the problem is not the tax system itself. It is the absence of a system that keeps records current, surfaces the tax liability in real time, and handles the submission process without requiring the business owner to understand the technical details of every HMRC requirement. Sage provides that system. The bank feed keeps the records current automatically. The tax estimate keeps the liability visible throughout the year. The expense categorisation captures every allowable deduction as it arises. The MTD quarterly submission goes to HMRC directly from the same interface where the daily bookkeeping happens.

The first tax return is only terrifying when you arrive at January with twelve months of unorganised records and no idea what you owe. It is manageable when you arrive at January with twelve months of organised, current, categorised records in Sage and a tax estimate you have been watching since April. The terror is a product of the process. Change the process and the terror largely goes away. That is what Sage does — not by making the tax system simpler, but by making the preparation so continuous and automatic that the deadline arrives as a confirmation rather than a revelation.