Hafiza Ayesha Waheed

Hafiza Ayesha Waheed

A VAT inspection from HMRC is not something most small business owners spend much time thinking about — until one arrives. Then it becomes very time-consuming, very stressful, and often expensive. What makes it worse is that the vast majority of problems HMRC finds during compliance checks are not the result of deliberate fraud. They are the result of avoidable, predictable mistakes that the right software would have caught or prevented entirely.

HMRC raised £5.3 billion from VAT investigations into UK businesses in 2024/25 alone. VAT inspection activity is rising, not falling — and a growing proportion of checks are being opened not because something obvious went wrong, but because HMRC’s own risk-scoring systems flagged a pattern that looked worth examining. This guide explains what those patterns are, why they keep recurring, and why the software you use to manage VAT is the most practical line of defence available to a UK small business.

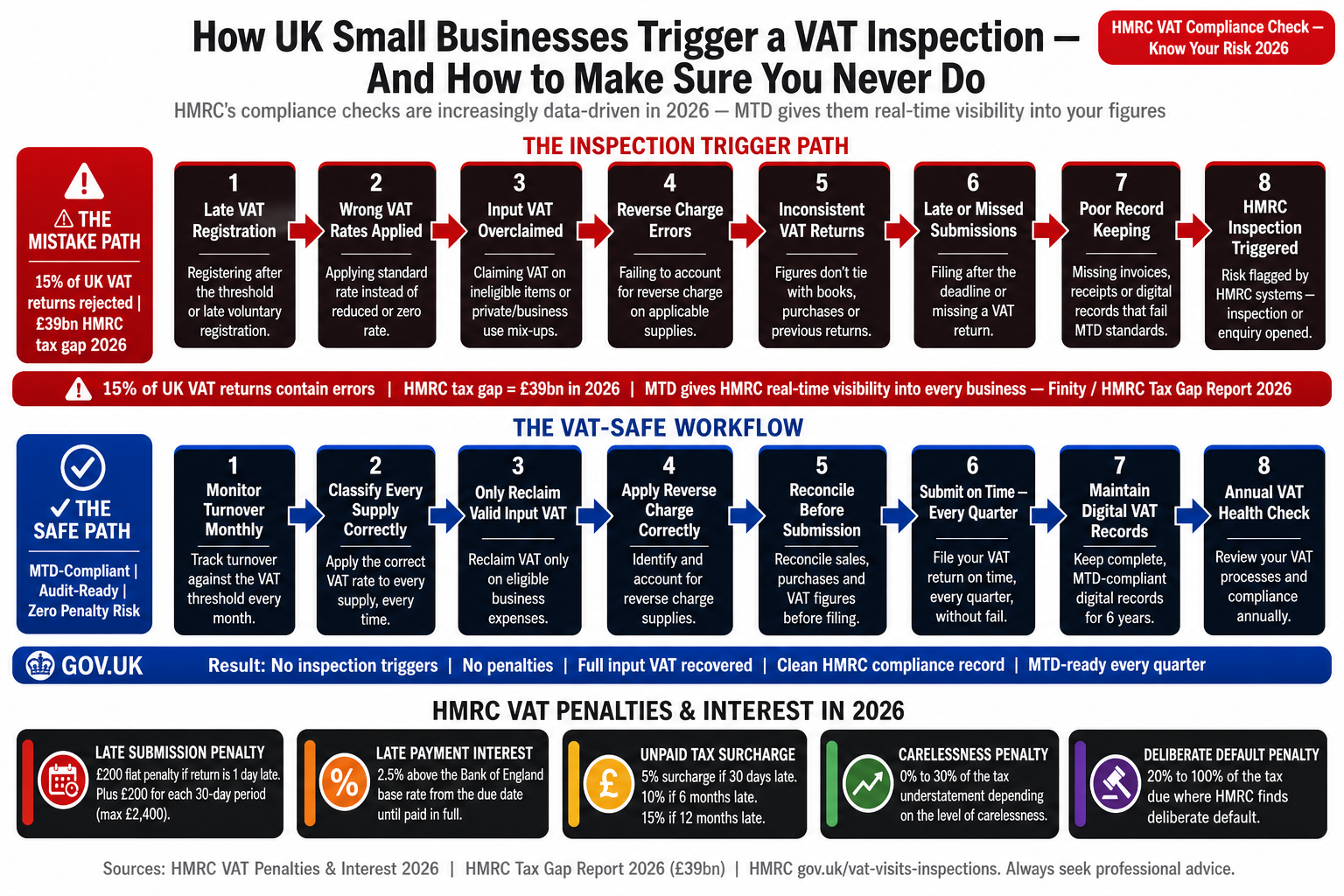

What Actually Triggers a VAT Inspection

HMRC selects businesses for VAT compliance checks through a combination of risk profiling, statistical modelling, and credibility checks on individual returns. Understanding what feeds that risk score is the starting point for understanding how to keep it low.

Trigger | Why HMRC Notices | How Common |

|---|---|---|

Late VAT returns or payments | Penalty points accumulate and flag the business for closer review | Very common |

Unusual repayment claims | A claim significantly above prior periods or sector norms triggers automatic review | Common |

Inconsistent figures across returns | Turnover declared for VAT does not match corporation tax or self-assessment records | Very common |

Credibility check failures | Input to output VAT ratios outside expected range for the sector | Common |

VAT registration delays | Business exceeded £90,000 threshold but registered late | Common |

High-risk sector | Construction, hospitality, and retail face elevated scrutiny | Sector-dependent |

Previous compliance failures | A business corrected before is more likely to be visited again | Common |

Third-party data mismatches | HMRC cross-references bank, Companies House, and payment processor data | Increasing |

Very few of those triggers require HMRC to suspect dishonesty. Most are simply signals of disorganisation — a business whose records do not tell a consistent, coherent story. That is a problem software solves directly, and it is why the choice of accounting platform matters more for VAT compliance than most business owners appreciate.

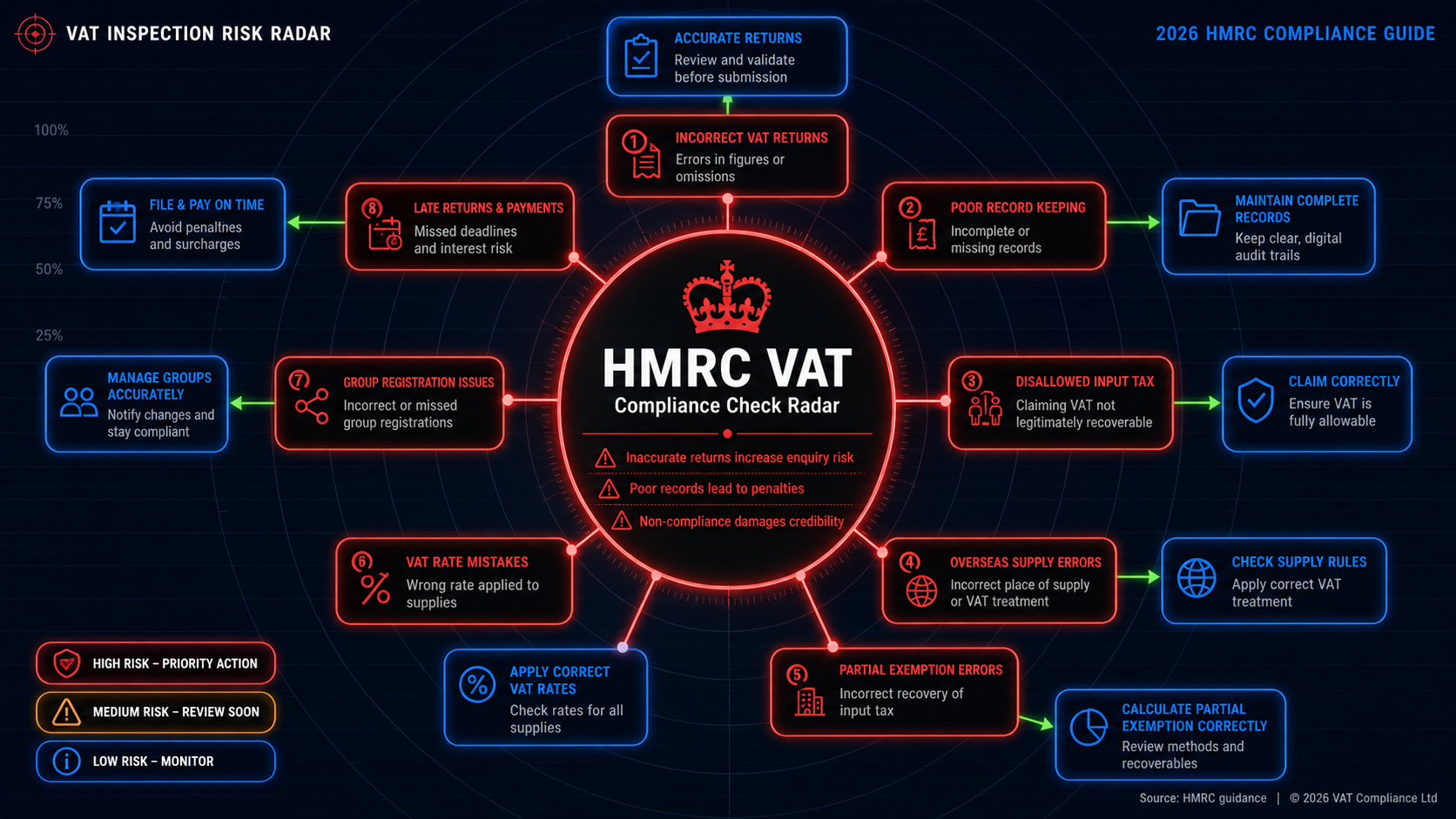

The Most Common Reasons Businesses Fail

When HMRC opens a compliance check and finds a problem, the problems cluster around the same categories every time. They are not exotic edge cases. They are errors that happen when VAT is managed reactively, without systems to catch mistakes before they become submissions.

Late Registration

The VAT registration threshold is £90,000 of taxable turnover in any rolling 12-month period — not the calendar year, not the financial year. A business that reviews figures annually may not notice it crossed the threshold in September until it files accounts the following spring. The cost of late registration is not just a fine. HMRC can require you to pay VAT on all sales made since you crossed the threshold, even if you never collected it from customers. For businesses with tight margins, that retrospective liability can be serious.

Broken Digital Links Under MTD

Since April 2022, all VAT-registered businesses must maintain a fully digital link from their records to their VAT submission. Copying a total from a spreadsheet and typing it into accounting software breaks the link. During an inspection, HMRC can trace the route from transaction to submission. A broken link is a compliance failure regardless of whether the final figures are accurate.

Wrong VAT Rates

The UK has three main VAT rates — 20% standard, 5% reduced, and 0% zero-rated — and the boundaries are not always intuitive. Food is largely zero-rated, but restaurant meals are standard-rated. Construction work falls across different rates depending on the property type. Applying the wrong rate is one of the most common errors HMRC encounters, and underdeclaring output VAT means repaying the full difference plus interest and penalties.

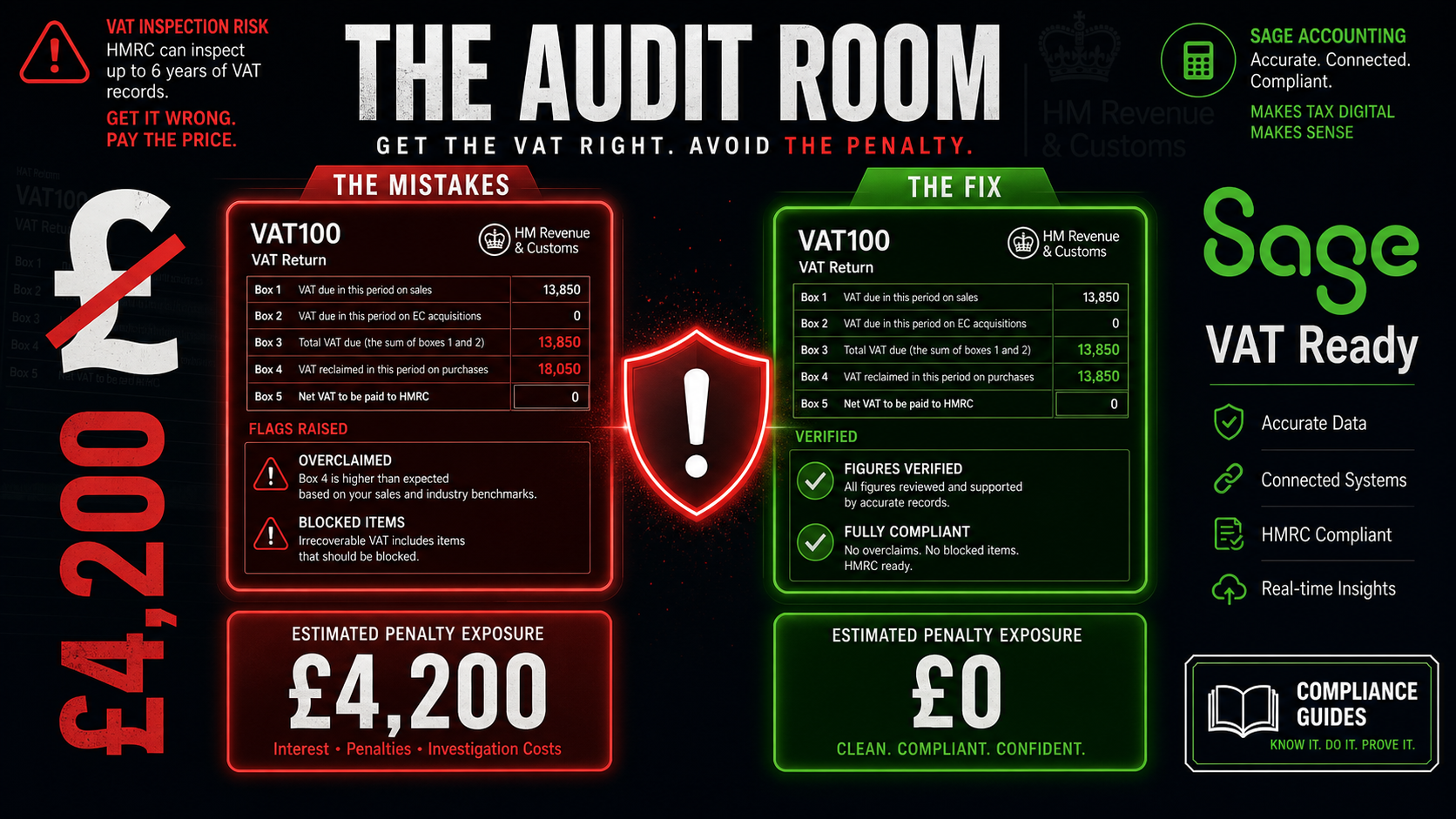

Incorrect Input VAT Claims

Input VAT can only be reclaimed on purchases used wholly or mainly for business purposes. Claiming on personal items, claiming without a valid VAT invoice, or reclaiming on blocked categories such as most car purchases are all common failure points. A bank statement alone is not sufficient evidence for a reclaim — HMRC requires the actual invoice.

The Construction Reverse Charge

The domestic reverse charge for construction services has been in force since 2021 and continues to cause errors. Under it, the VAT liability shifts from supplier to customer. A subcontractor within CIS scope must not charge VAT — the main contractor accounts for it instead. Misapplication creates visible mismatches when HMRC compares supply chain data.

The Penalty System in 2026

HMRC replaced the old VAT surcharge system with a points-based model for late submissions and a percentage-based model for late payment. Both apply from VAT periods starting 1 January 2023 and operate independently.

Situation | Penalty | Notes |

|---|---|---|

Late VAT return | One penalty point added | No financial penalty until threshold reached |

Quarterly filer hits 4 points | £200 financial penalty | Each further late submission adds another £200 |

VAT paid 1–15 days late | No penalty if paid within 15 days | Grace period on first occurrence |

VAT paid 16–30 days late | 2% of outstanding VAT | Calculated on amount unpaid at day 15 |

VAT paid 31+ days late | 4% annualised rate, daily | Compounds until paid in full |

Careless inaccuracy | 0–30% of lost revenue | Reduced for unprompted disclosure |

Deliberate inaccuracy | 20–70% of lost revenue | Higher if concealed; reduced for disclosure |

The disclosure advantage

Businesses that report their own errors to HMRC before an inspection is opened consistently receive lower penalties than those where HMRC finds the problem first. Most accounting software surfaces discrepancies that make self-correction practical. Acting on those signals is always the better calculation.

What HMRC Looks at During a Check

A VAT compliance check can be a desk review by letter or a full in-person visit. In both cases, HMRC wants to verify that the returns submitted accurately reflect actual transactions. The businesses that emerge cleanly are the ones whose records are organised enough that any question can be answered quickly — that clarity reduces the investigation scope, shortens the timeline, and influences the penalty level if a correction is needed.

Sales invoices must show your VAT number, the rate applied, and the VAT amount separately from the net figure

Input VAT claims must be backed by valid VAT invoices stored in your records — bank statements are not sufficient

A VAT account showing running output and input VAT through the period must exist and tie to the return submitted

Any non-standard treatment — partial exemption, reverse charge, zero-rating — must be documented and explainable

The digital link from records to submission must be demonstrably intact, not just described as intact

How the Right Software Prevents Most of This

The digital link problem disappears entirely with proper accounting software. When your bank feed connects directly to your platform and flows through to your VAT return without any manual transfer, the unbroken chain MTD requires exists by design. Sage connects to all major UK banks and challengers via Open Banking, with the audit trail from transaction to return built into every submission automatically.

VAT rate application becomes systematic. Every product and service carries a coded rate. Once set, it applies to every transaction of that type — eliminating the category of error that comes from assigning rates by hand. The difference between coding rates once and assigning them transaction by transaction is the difference between one decision and hundreds.

Threshold monitoring removes late registration risk entirely. Sage Copilot monitors your rolling 12-month income continuously and flags when the £90,000 VAT registration threshold is approaching — without requiring you to run a report to find out. A business tracking turnover in real time never misses the registration window.

Every transaction in Sage carries a timestamp, a user record, and a link to supporting documents. Every return carries a complete trail back to the transactions behind it. When HMRC asks for evidence behind Box 4 of your return, the answer is a filter on a live database, not a search through folders. That audit trail reduces both the stress and the financial risk of any compliance check.

What a VAT-Ready Business Looks Like

High VAT inspection risk

Returns filed manually or via spreadsheet with no software audit trail

VAT rates assigned transaction by transaction, not systematically

Rolling 12-month turnover reviewed annually rather than continuously

Input VAT claimed on bank statements rather than valid VAT invoices

Figures manually combined from multiple spreadsheets before submission

Late returns on a recurring basis, accumulating penalty points

No documented process for reverse charge in construction

Low VAT inspection risk

All transactions in HMRC-recognised software with unbroken digital link to each return

VAT rates coded to products and services — applied automatically every time

Rolling turnover monitored continuously with built-in threshold alerts

Input VAT claimed only against invoices matched within the accounting system

Bank feed connected directly — no manual transfer of figures

Returns filed on time, every period, with confirmation on record

Reverse charge handled through a native workflow in software

Sage and VAT Compliance

Among HMRC-recognised platforms, Sage is built around UK compliance requirements as a foundation rather than an add-on. The VAT return in Sage is a calculated output from records kept throughout the period, submitted directly to HMRC via the MTD API with a full audit trail. No manual form. No re-entry of figures. No separate submission tool.

Sage Copilot extends this into proactive monitoring — flagging transactions coded at unexpected VAT rates, input claims without matching invoices, and income approaching compliance thresholds, without waiting for you to run a report. For a business owner who is not thinking about VAT every day, that background monitoring is the difference between catching a problem in week two of a quarter and discovering it during an HMRC enquiry six months later.

For construction businesses, Sage handles the domestic reverse charge natively. The workflow is built into invoicing and purchase recording, ensuring subcontractors issue correctly and main contractors account for the VAT shift without a separate manual step. For a sector HMRC scrutinises heavily, native integration is a material compliance advantage.

Sage also offers UK phone support on all paid plans. For a business heading into a quarter with a large repayment claim or an unusual transaction, the option to call someone rather than search a knowledge base is worth factoring into the software decision before something goes wrong.

The Bottom Line

HMRC’s VAT compliance activity is intensifying. Its risk-scoring tools cross-reference VAT returns against bank data, company filings, and payment processor records in ways that manual bookkeeping cannot keep pace with. A business managing VAT reactively, on spreadsheets, with no real-time monitoring, is carrying more inspection risk than it likely realises — and will be the last to know.

Most VAT inspection failures are not dishonesty. They are the result of systems that were not good enough to catch avoidable mistakes. That is a problem the right software solves before HMRC ever sends a letter — and solving it in advance is a considerably less stressful way to stay compliant than finding out what your records look like only after an officer asks to see them.