Hafiza Ayesha Waheed

Hafiza Ayesha Waheed

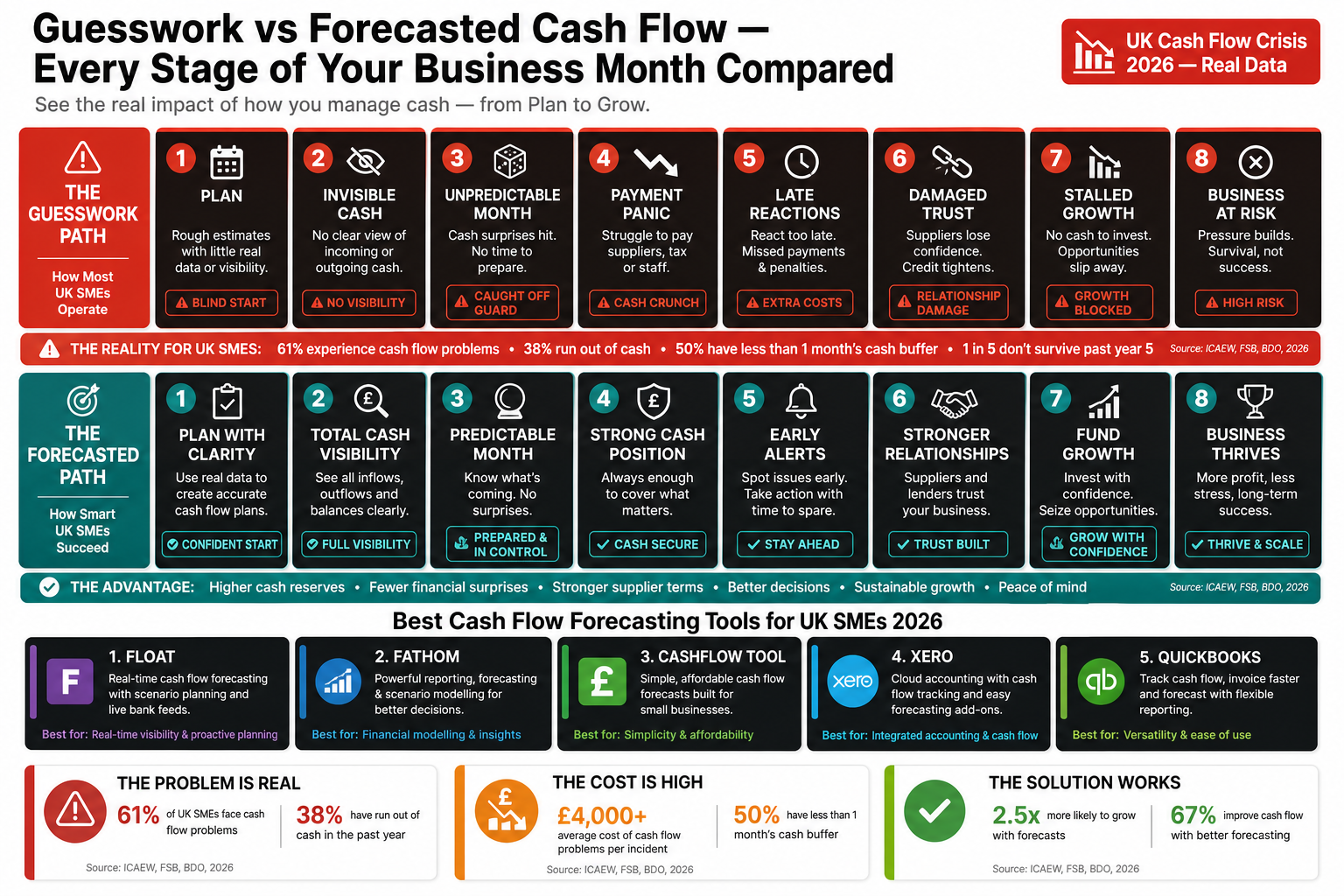

Ask a UK small business owner what they think will happen to their bank balance next month, and the honest answer is usually a shrug. They know roughly what is coming in. They know roughly what needs to go out. Everything in between is hope, habit, and a daily check of the account balance to confirm nothing catastrophic has happened overnight. That is not cash flow management. It is cash flow guessing — and it is the operating model for the majority of UK small businesses right now, with consequences that show up repeatedly in the insolvency data.

The proof that guessing is not working is not hard to find. 82% of UK business failures are directly attributed to poor cash flow management — not bad products, not insufficient customers, not market conditions. Cash flow. And nearly half of all UK SMEs reported cash flow challenges in the last 12 months, with 10% of those saying the pressure was severe enough that they were actively considering closure. These are not struggling businesses in struggling markets. Many of them are profitable, busy, and growing. They simply cannot see what is coming — and that invisibility is costing them.

What Guessing Actually Costs

The cost of managing cash flow without a forecast is not abstract. It shows up in specific, measurable ways: emergency overdraft fees incurred because a VAT bill landed at the same time as two large supplier invoices. A growth opportunity declined because there was no visibility on whether the business could fund the upfront cost. A bank loan application rejected because the business could not demonstrate a credible cash flow projection. A hire delayed by three months because nobody knew whether the salary was sustainable beyond the next quarter.

Each of those outcomes has a number attached to it. Overdraft fees for small businesses typically run at 15% to 20% EAR for unauthorised borrowing — far higher than a planned facility arranged in advance. Declined growth opportunities are harder to quantify but consistently cited by UK SME owners as one of their largest regrets. The British Business Bank’s 2025/26 Small Business Finance Markets report found that access to finance remains a persistent barrier for UK SMEs, with poor cash flow visibility identified as one of the primary reasons applications fail — not insufficient revenue, but insufficient forward-looking data.

The number behind the guessing

82% of UK business failures are caused by poor cash flow management. Not bad products. Not too few customers. Cash flow. Almost all of those failures were businesses that were trading, invoicing, and collecting — but doing it without being able to see far enough ahead to act before a gap became a crisis.

The State of UK SME Cash Flow in 2026

The 2026 data paints a consistent picture of a business environment where cash flow pressure is widespread, structural, and in most cases not the result of underlying weakness. According to Intuit QuickBooks’ Quarterly Small Business Insights Survey of 980 UK SME owners, 47% are already experiencing cash flow pressures, and 57% expect their costs to rise further in the next quarter. Of those expecting rising costs, 64% expressed direct concern about the operational impact. Nearly a third reported that financial visibility — or the lack of it — was a primary barrier to growth.

The Coface 2025 UK Payment Survey adds a crucial layer: 90% of UK businesses experienced late payments in 2025, a higher rate than France (85%), Germany (81%), or Poland (60%). The average payment delay stands at 32 days beyond the due date — consistent across company sizes but with disproportionate impact on micro and small businesses, where nearly 50% reported experiencing delays more frequently than in previous years. When 90% of businesses face late payments and the average delay is a full month, the cash flow gap between what the P&L shows and what the bank account holds is not an anomaly. It is a structural feature of operating as a small business in the UK in 2026.

Metric | Figure | Source |

|---|---|---|

Business failures caused by poor cash flow | 82% | Approved Business Finance, 2026 |

UK SMEs with active cash flow pressures | 47% | Intuit QuickBooks SMB Insights, 2025 |

SMEs expecting rising costs next quarter | 57% | Intuit QuickBooks SMB Insights, 2025 |

SMEs struggling, considering closure | ~10% of those with cash flow issues | Shawbrook / Bridging & Commercial, 2025 |

UK businesses facing late payments | 90% | Coface UK Payment Survey, 2025 |

Average payment delay beyond due date | 32 days | Coface UK Payment Survey, 2025 |

SMEs citing financial management as barrier to growth | 51% | Intuit QuickBooks SMB Insights, 2025 |

Hours spent chasing late payments per year | 133 million (all UK SMEs combined) | UK Government / ACCA, March 2026 |

UK corporate insolvencies in 2025 | 28,616 | R3 / Insolvency Service, Jan 2026 |

Why Spreadsheets Are Not the Answer

The default response to “we need to manage cash flow better” is to build a spreadsheet. And for a business with three customers, one bank account, and predictable monthly costs, a spreadsheet might be adequate. For any business more complex than that, a manually maintained cash flow spreadsheet has a specific set of failure modes that make it less reliable than it feels.

First, it is only as current as the last time someone updated it. A spreadsheet that was accurate last Tuesday is not accurate today if three invoices have been paid, one large supplier payment has gone out, and a VAT quarter has closed. Every day without an update is a day in which the forecast diverges from reality. Second, it does not connect to anything. The accounts receivable position in the accounting system and the expected inflows in the spreadsheet are maintained separately, manually reconciled on whatever schedule the owner can manage. That gap is where errors enter. Third, it cannot model scenarios at speed. Changing one assumption — what if this customer pays 30 days late? — requires manual recalculation of every downstream figure. In practice, scenario testing does not happen at all.

The businesses that have moved from spreadsheets to integrated forecasting tools consistently report the same thing: it is not that the spreadsheet was wrong. It is that the spreadsheet required active maintenance to stay right, and the moment that maintenance slipped — because the owner was busy, because it was month-end, because a crisis intervened — the forecast became a historical document rather than a live management tool. G2 reviewers of Futrli by Sage describe it plainly: “Cash flow is now easy to produce in a matter of minutes. This saves hours if not days of manual work.”

What a Real Forecast Actually Shows You

A functioning cash flow forecast does not just show whether the business will have money. It shows when it will have money, how much, and what the bank balance will look like on any specific date based on current and expected transactions. That granularity is what turns a forecast from a planning exercise into an operational tool.

The standard for most UK SMEs between £1 million and £30 million in revenue is a rolling 13-week forecast updated weekly, supported by a 12-month outlook updated monthly. The 13-week window covers the operational planning horizon — the period within which most payment and expenditure decisions need to be made. The 12-month view provides the strategic context: seasonal patterns, major outgoings, tax obligations, and growth-related expenditure. Together they answer the two questions that matter most: what do we need to do this week, and what do we need to plan for this quarter.

Week-by-week bank balance projections — not a monthly average, but the actual expected balance on any given day, showing when it dips and by how much

VAT and PAYE liabilities as visible future outflows — not surprises that arrive at quarter end but planned events with a known cash requirement built into the projection

Scenario modelling — what happens to the balance if a major customer pays 30 days late; what happens if a planned equipment purchase is brought forward; what happens if a new hire starts in March rather than May

Aged debtor integration — outstanding invoices feeding directly into expected inflows, with overdue amounts flagged as at-risk rather than assumed settled on their original terms

Seasonal pattern recognition — identifying recurring dips before they arrive, giving time to build reserves or arrange temporary facilities in advance

How Sage and Futrli Make This Automatic

The reason most UK small businesses do not have a functioning cash flow forecast is not that they do not understand its value. It is that building and maintaining one manually competes with every other demand on the owner’s time, and the maintenance always loses. Sage’s cash management tools, and Futrli by Sage for businesses that need more advanced forecasting, remove the maintenance problem by building the forecast from live transaction data rather than manual inputs.

In Sage Accounting, the cash flow forecast is generated directly from the data already in the system — invoices raised, payments received, bills entered, bank transactions matched. The forecast updates automatically as the underlying data changes. There is no separate spreadsheet to maintain, no reconciliation step between the accounting records and the forecast model, and no risk of the two diverging because someone was too busy to update the projection. The bank balance tomorrow is calculated from the transactions entered today.

Futrli by Sage extends this with three-way forecasting — linking the cash flow forecast, the profit and loss projection, and the balance sheet into a single connected model. When a sales forecast changes, the cash flow and balance sheet update automatically. When a large expense is entered, all three statements reflect the impact immediately. For businesses preparing for a bank funding application, an investor conversation, or a period of planned growth, three-way forecasting provides the credible, integrated financial projections that those conversations require — built from live accounting data, not assembled manually from separate sources.

Guessing vs. Forecasting: The Real Difference

Guessing (no forecast)

Check the bank balance daily and react to what you see

VAT bill arrives at quarter end — assess whether funds are available on the day

Late payment from a customer discovered when balance drops unexpectedly

Growth opportunity evaluated based on current balance, not projected position

Seasonal cash dip noticed when it is already happening

Bank or investor asks for cash flow projection — spend two days building one from scratch

Tax liabilities — Corporation Tax, PAYE — felt as shocks rather than planned events

Overdraft used reactively; facility cost higher than a planned arrangement

Forecasting with Sage

Rolling 13-week balance projection updated automatically from live transaction data

VAT liability visible as a known future outflow from day one of the quarter

Overdue invoices flagged in the aged debtor report before they affect the projection

Growth decision modelled against projected cash position, not current balance

Seasonal pattern identified 6–8 weeks out; reserves built in advance

Three-way forecast available instantly from live Sage data; investor-ready in minutes

All known liabilities modelled in; no surprises that the data could have predicted

Planned facility arranged before it is needed; cost materially lower

The Futrli Feature Set

Feature | What It Does | Why It Matters |

|---|---|---|

3-way forecasting | Links P&L, balance sheet, and cash flow into one connected model | Any change in one statement flows through automatically; no manual reconciliation |

Scenario planning | Build and compare multiple versions of the forecast side by side | Test best/worst case before committing to a decision; choose the plan with confidence |

Auto-predictions | Rapidly generated forecasts based on historical transaction patterns | Forecasting starts from a realistic baseline rather than a blank sheet |

VAT & tax modelling | Automatically calculates and includes VAT, PAYE, and corporation tax as future outflows | Eliminates the end-of-quarter tax shock; liability visible from the start |

Invoice repayment dates | Adjustable expected payment dates for invoices due; models late payment impact | Provides realistic inflow projections rather than optimistic on-time assumptions |

HR forecasting | Models the impact of hiring decisions including salary, NIC, and pension | Hire with confidence; see the cash impact of a new employee before making the offer |

60+ reporting templates | Automated, branded reports for clients, investors, and banks | Investor-ready financials produced in minutes from live Sage data |

Traffic-light predictions | Visual indicators flagging projected cash shortfalls and surpluses | Problems visible at a glance; no need to read through rows of figures to find the risk |

When Forecasting Changes the Decision

The value of a cash flow forecast is not in the document. It is in the decisions it changes. A business that sees a projected negative balance in week nine has options in week three that it does not have in week eight. Those options — negotiating an early payment from a customer, arranging a short-term facility, deferring a planned purchase, adjusting payment terms with a supplier — all require lead time. None of them are available when the bank balance is already negative and the payroll run is 48 hours away.

The same principle applies to growth decisions. A business considering taking on a large new contract needs to know whether it can fund the upfront costs before the revenue arrives. Without a forecast, that question is answered by checking the current balance and making an optimistic assumption about timing. With a forecast, it is answered by modelling the contract’s cash impact against the projected position, including all other known inflows and outflows, and seeing exactly what the balance looks like at each point in the delivery cycle. That is the difference between a growth decision made with confidence and one made with hope.

The 69% of accountants who say financial forecasting is critical to their clients’ businesses — the figure cited directly by Sage and Futrli — are not expressing a preference for financial complexity. They are reflecting a consistent observation: the businesses that survive cash pressure are the ones that see it coming. The businesses that do not survive are often the ones that were surprised by something a forecast would have shown them weeks earlier.

The Bottom Line

Cash flow does not have to be a guessing game. The data is unambiguous: 82% of UK business failures trace back to cash flow mismanagement, 47% of UK SMEs are under active cash flow pressure right now, and 90% face late payments from customers as a structural feature of operating in the UK market. The businesses that navigate all of that are not doing something heroic. They are doing something systematic: they know what their bank balance will look like in three weeks, in six weeks, and in three months, and they act on that information before problems arrive rather than after.

Sage provides the foundation for that visibility — live transaction data, an automatically updated cash flow statement, and aged debtor reporting that shows what is owed and when it is at risk. Futrli by Sage extends it into full three-way forecasting, scenario modelling, and investor-ready reporting, built from the same live data without requiring any additional manual input. For a UK small business owner who is currently managing cash flow by checking the bank balance and hoping, both of those tools represent the same thing: the replacement of guessing with knowing.

The businesses that made it through the 28,616 corporate insolvencies of 2025 intact were not uniformly larger, better funded, or more profitable than those that did not. They were, in a consistent pattern, better informed about what was coming. That information is no longer a privilege of businesses with dedicated finance teams. It is available, in Sage, to any UK business owner who decides to stop guessing.